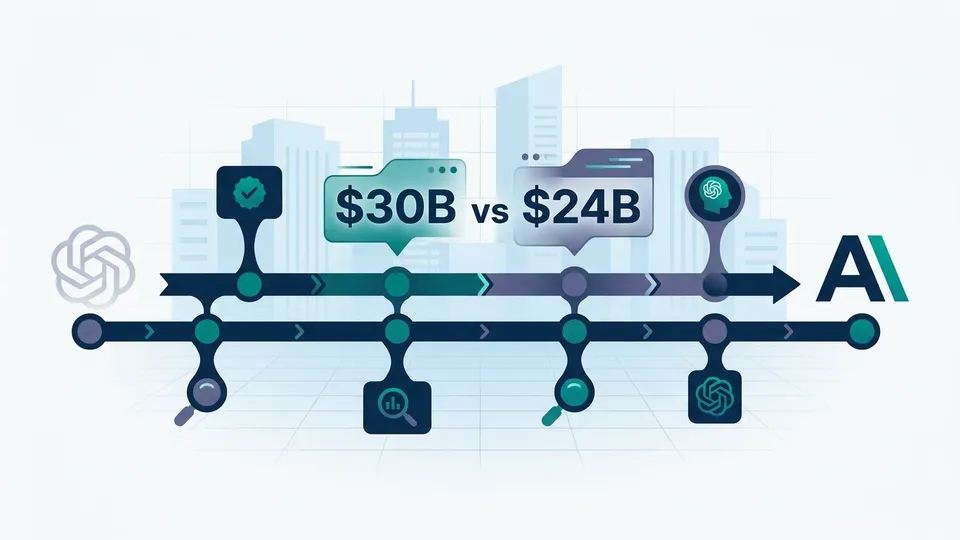

The AI That Out-Earns ChatGPT: Anthropic's $30B ARR and the Enterprise Power Shift

Anthropic's ARR hit $30B, passing OpenAI's $24B. Breaking down the enterprise flip, the 80% B2B revenue structure, 4x training cost efficiency, and what it means for your AI tool selection.

What you'll learn in this article

- The key point to grasp before reading the full article

- How the issue changes practical decisions after reading

- Which follow-up article is worth opening next

Which company is making more money — the one behind ChatGPT, or the one behind Claude?

In April 2026, that answer flipped. Anthropic’s ARR (Annual Recurring Revenue) reached $30 billion, surpassing OpenAI’s $24 billion for the first time (Sherwood News).

“But ChatGPT has way more users?” — that’s exactly the right question. OpenAI wins decisively on user count. And yet it’s now trailing in revenue.

I call the reason behind this reversal the “Enterprise Flip” — the transition from the era of consumer chat AI to the era of enterprise agent AI. The shift in AI industry gravity, finally made visible in the numbers.

In this article I break down the $30B ARR from five angles, then distill the implications into three criteria for choosing which AI to bet on.

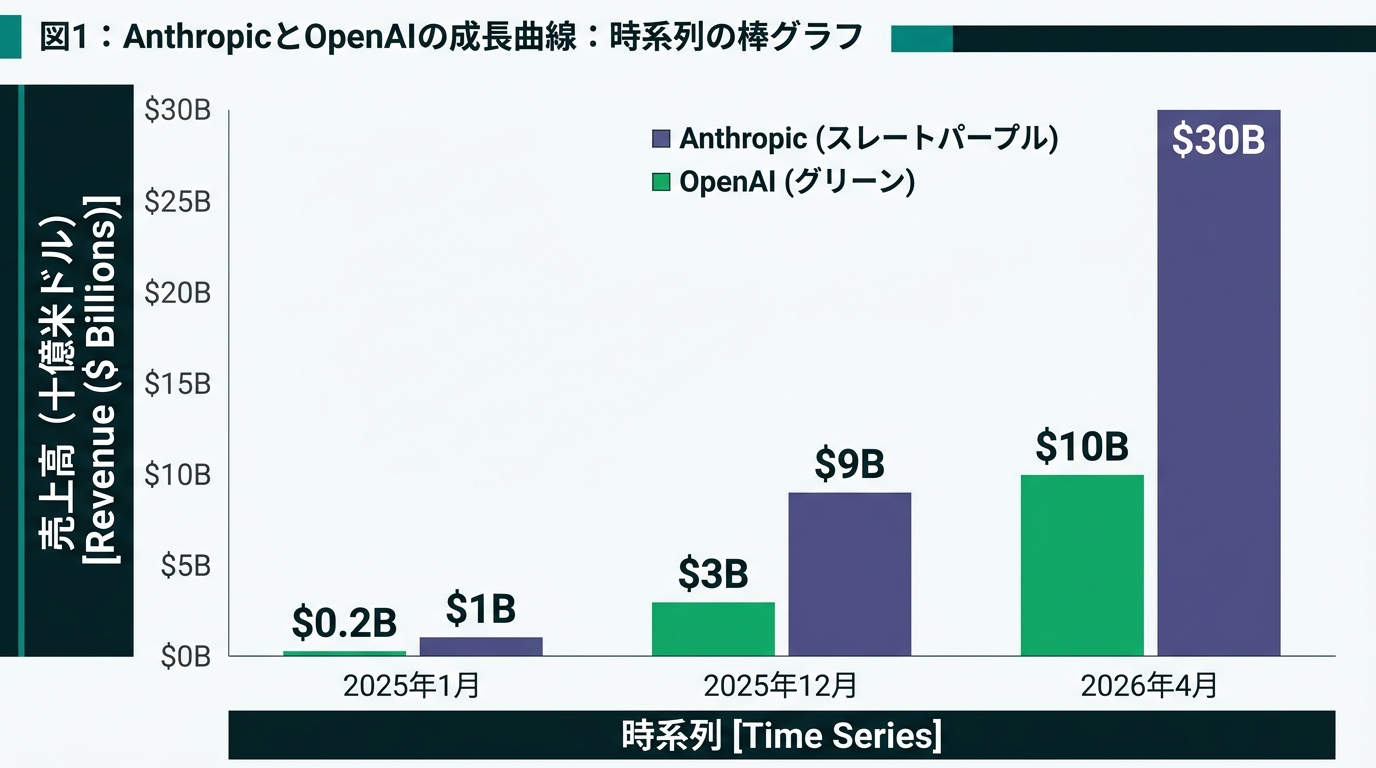

30x in 15 Months: The $30B ARR in Full

Anthropic grew ARR from $1B to $30B in 15 months, taking the revenue lead in AI.

The timeline: $1B in January 2025. $9B by year-end. $30B by April 2026 (SaaStr).

Getting from $1B to $9B took 11 months. Getting from $9B to $30B took just 4 months. The late acceleration is remarkable. The explanation: enterprise contracts started compounding. AI adoption crossed from “experiment” to “required investment for competitive survival.”

OpenAI’s monthly revenue runs at $2B, equating to $24B annualized. Whether the $6B gap is temporary or structural becomes clear when you look at what’s inside the revenue.

80% Enterprise Revenue: The Structural Difference That Defines the Flip

80% of Anthropic’s revenue comes from enterprise customers. OpenAI is primarily consumer subscription-driven. This structural gap is the Enterprise Flip.

Side-by-side comparison:

| Metric | Anthropic | OpenAI |

|---|---|---|

| ARR | $30B | $24B |

| Revenue driver | Enterprise 80% (PYMNTS) | Consumer subscription-centric |

| $1M+ annual customers | 1,000+ (IndexBox) | Not disclosed |

| Annual training cost (2030 projection) | $30B | $125B |

| Breakeven projection | 2027 | 2030 |

Three reasons enterprise-centric is a structural advantage:

Unit economics are an order of magnitude different. Individual: $20/month. Enterprise: $80K–$1M+/year. A single contract generates what thousands of individual subscriptions would.

Churn is structurally low. When AI is embedded into workflows, switching costs skyrocket — rewriting code, retraining staff, rebuilding data connections. Completely different from an individual deciding “I’ll cancel this month.”

Usage naturally expands. One department proves ROI → company-wide rollout follows. The 500 companies that became 1,000 in two months ran on internal word-of-mouth compounding.

Training Cost at One-Quarter: The Efficiency Model That Changes the P&L

Anthropic’s AI model training costs are roughly one-quarter of OpenAI’s — a fundamental efficiency advantage that reshapes the profitability trajectory.

Wall Street Journal estimates annual training costs through 2030 at $125B for OpenAI and $30B for Anthropic (SaaStr). A 4x+ gap.

With similar revenue and a quarter of the costs, the profit picture is completely different. Think of two ramen restaurants with the same annual revenue — the one with a quarter of the ingredient costs will be four times as durable in five years. The same structural logic applies in AI.

This efficiency gap stems from design philosophy. Anthropic’s DNA is “safe and efficient.” Not building the biggest model with maximum compute, but extracting required performance with minimum resources. In March 2026, partnerships with Google and Broadcom also secured gigawatt-scale compute infrastructure (Anthropic official).

The result: Anthropic projects free cash flow breakeven in 2027. OpenAI’s breakeven is 2030. A 3-year lead — and as investors shift focus from ARR growth rate to “when does it turn profitable,” that 3-year difference is a substantial competitive advantage.

$380B Valuation and IPO: What Investors Are Actually Buying

February 2026 Series G at $30B raise, $380B valuation. Q4 2026 IPO likely. Investors are buying “the infrastructure of the agent economy.”

In February 2026, Anthropic closed a Series G of $30B, led by GIC (Singapore’s sovereign wealth fund) and Coatue. Post-money valuation: $380B (CNBC).

$380B exceeds Toyota and Sony, the largest manufacturing names in Japan — an unprecedented valuation for a four-year-old company. The P/S ratio (price to ARR) is approximately 12.7×. Investors aren’t looking at today’s revenue; they’re buying Anthropic’s position as the infrastructure of the AI agent ecosystem. History has already shown what happens to companies that capture platform positions — AWS and Salesforce being the clearest examples.

For IPO timing, SeekingAlpha analysis points to October 2026 as most likely (Seeking Alpha). Going public means quarterly earnings disclosures — the question “are AI agents actually being used?” will finally be answered in public numbers. $380B is the market’s stated conviction.

Agentic AI Is What Opened the Enterprise Wallet

The reason 1,000+ companies each pay $1M+ annually isn’t chat subscriptions — it’s investment in infrastructure that works autonomously.

Interpreting “$1M+/year enterprise customers” as “paying to chat with AI” misses the point entirely. What enterprises are buying is the foundation for agents that run work autonomously.

The April 2026 release of Claude Managed Agents symbolizes this (Anthropic official). A framework for deploying, monitoring, and scaling AI agents in the cloud. Three domains in transformation:

- Customer support: Autonomous completion from inquiry analysis through refund processing. Humans focus only on exception cases.

- Software development: Code review, test execution, and documentation generation handled by agents. Developers focus on design and decision-making.

- Data analysis: 24-hour agents handling routine reports and anomaly detection automatically. Analysis complete when you arrive in the morning.

Many AI pilot projects failed against infrastructure barriers. Managed Agents was designed to remove those barriers. Rakuten and other early adopters are already in production.

I run my own AI agent system (Izumo) daily. The gap between “asking AI questions” and “delegating work to AI” is total. Once you make that transition, going back is nearly impossible. That irreversibility is why enterprises pay $1M+.

Which AI to Bet On: 3 Business Criteria

AI selection is a business design problem, not a preference. The Enterprise Flip gives us 3 evaluation criteria.

The era of picking based on “which AI is smarter, ChatGPT or Claude?” is over. Working backward from business requirements is the only correct approach.

| Criterion | ChatGPT direction | Claude direction |

|---|---|---|

| Use case | Individual chat, self-contained UI work | API integration, team workflow automation |

| Cost design | Simple $20 × headcount fixed-cost management | Usage-based API billing for medium/long-term optimization |

| Agent support | Expanding capabilities (as of April 2026) | Managed Agents active, mature ecosystem |

One clarification: this isn’t a claim that ChatGPT is inferior. For personal use and writing tasks, ChatGPT remains optimal in many scenarios. The point is to stop choosing based on “I like it” or “it’s famous” and start working backward from how your organization actually works.

“Am I using this personally, or embedding it in my team’s systems?” — decide this one question first. Once it’s clear, the options narrow naturally.

Summary: What to Start Doing in the Enterprise Flip Era

Anthropic $30B, OpenAI $24B. The numbers reflect structural change. AI industry revenue shifted from “individual chat subscriptions” to “enterprise agent operations.”

The Enterprise Flip didn’t happen overnight. Enterprise customers making up 80% of revenue, 1,000+ companies each paying $1M+, breakeven 3 years ahead of the nearest competitor, $380B valuation — this combination has no precedent in the AI industry.

I work with AI agents every day. Moving from “the stage of asking AI questions” to “the stage of running work with AI” changes the productivity dimension entirely. It’s a feeling you can only understand by experiencing it — which is why I keep recommending people just try it.

Three things you can start today:

- Write out 3 “repeating tasks” in your daily work. Email replies, data aggregation, report generation. That’s the starting point for agentic automation. Just articulating “what can AI take over?” changes what you see.

- Automate one task using the Claude API free tier. Without touching it, you have no information to make a decision. Start small, decide from experience. The moment the first one works, the conviction of “this can work” clicks in.

- Redesign your 6-month AI budget as “agent infrastructure investment.” The $30B ARR proves that 1,000+ companies have already made that decision. Organizations that move faster accumulate agent operation expertise first.

The Enterprise Flip has already happened. 1,000+ companies have already moved. You’re next.

AIを使いこなせない方は、この先どんどん差がつきます。僕はAIエージェントを毎日動かして、壊して、直して、また動かしてます。そういう泥臭い実践の記録をここに書いてます。理論は他の方にお任せしました。僕は動くものを作ります。朝5時に起きてウォーキングしてからコードを書くのがルーティンです。